As leaders, we know that fraud and risk are no longer just defensive functions. They are strategic levers that, when designed thoughtfully, can fuel growth and strengthen the resilience of our organizations. Too often, however, fraud and risk management become afterthoughts—addressed only when losses mount or regulatory pressure increases. By then, the cost of catching up is far greater than the cost of planning ahead.

In my experience working with financial institutions at different stages of growth, one thing is clear: the way you structure your fraud and risk teams will define how effectively you can navigate an increasingly complex threat landscape. From fraud and cybersecurity to compliance and credit risk, each area requires specialized expertise, but together they form the foundation for trust, customer experience, and long-term success.

In this article, I will share the most common organizational models we see today, highlight their strengths and challenges, and outline the mindsets and skills that make them work. My goal is to provide a practical framework you can use to evaluate your own setup—so that fraud and risk not only protect your business, but also become true strategic assets for growth.

The Four Biggest Risks Facing Financial Institutions Today

Financial institutions today operate in an environment where risks are multiplying and evolving faster than ever. Fraud, cyberattacks, compliance obligations, and credit exposure each present distinct challenges—and together they form a complex web that can hold back growth if not addressed proactively.

Fraud Risk. Fraud remains one of the most immediate and visible threats. From account takeovers and payment fraud to promotion abuse and synthetic identities, fraudsters constantly adapt their methods. Left unchecked, fraud leads to direct financial losses and erodes customer trust.

Cybersecurity Risk. Data breaches and sophisticated attacks have become the norm rather than the exception. A single incident can compromise sensitive information, damage reputations, and expose organizations to cascading fraud attempts downstream.

Compliance Risk. For financial services organizations, compliance is non-negotiable. Regulators expect robust anti-money laundering (AML) and counter-terrorist financing (CTF) programs, along with detailed reporting and monitoring. Falling behind in compliance doesn’t just bring fines—it can jeopardize licenses and long-term viability.

Credit Risk. For lenders and issuers, credit risk is a fundamental concern. Extending credit while minimizing default requires balancing opportunity with prudence, a challenge that grows as new lending models (such as BNPL) proliferate.

As companies scale, these risks only become more pronounced. Too often, organizations discover that while their business has grown quickly, their fraud and risk structures have lagged behind. The result: financial losses, regulatory setbacks, and operational inefficiencies that could have been avoided with the right foundation.

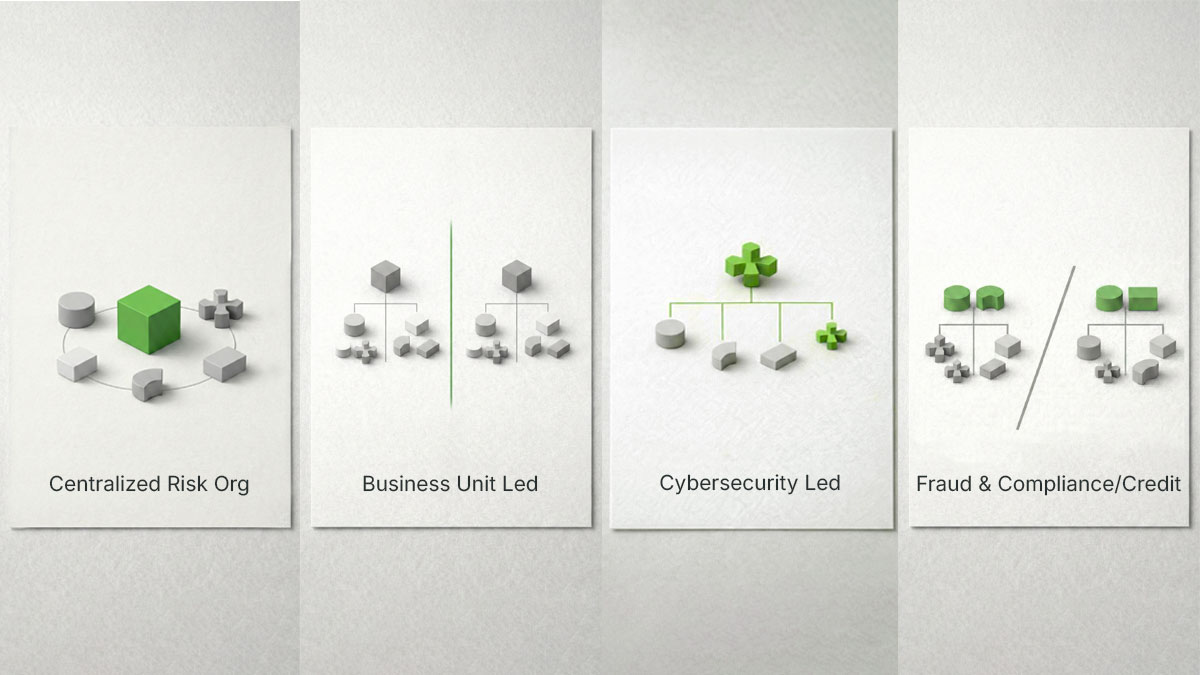

Common Fraud and Risk Organization Structures

When it comes to designing a fraud and risk organization, there is no single “right” answer. Different companies adopt different structures depending on their stage of growth, business complexity, and regulatory environment. Over the years, I’ve observed four primary models that financial institutions tend to follow—each with unique strengths and challenges.

Centralized Chief Risk Officer (CRO) Model

In this setup, a single Chief Risk Officer oversees all risk functions, from fraud and cybersecurity to compliance and credit.

- Strengths: Unified risk visibility, stronger executive alignment, efficient resource sharing, and clear accountability.

- Challenges: Finding a CRO with broad expertise is difficult, business units may feel disconnected from risk decisions, and some risk areas can get overshadowed by others.

Business Unit–Led Risk Teams

Here, each business unit owns its own fraud and risk management, tailoring it to its specific needs.

- Strengths: Deep alignment with business priorities, faster decision-making, and specialized expertise for each unit.

- Challenges: Risk teams may become siloed, customer experience can be inconsistent across products, and costs rise due to duplicated tools and efforts.

Cybersecurity-Led Fraud Functions

Some organizations combine fraud with cybersecurity under a single leader, often the Chief Information Security Officer.

- Strengths: Strong perimeter defense, unified tools and authentication strategies, and close alignment with IT.

- Challenges: Fraud detection skills are often different from cyber talent skills , thus sometimes leaving gaps in analytics, transaction monitoring, and proactive fraud detection.

Combined Fraud and Compliance Teams (or Fraud and Credit Teams)

Increasingly, organizations place fraud and compliance (or credit) under the same umbrella, often reporting to a common VP or C-level Officer.

- Strengths: Shared infrastructure and data, a holistic view of risks, and closer alignment with regulatory needs.

- Challenges: Balancing different goals (loss prevention vs. compliance/reporting obligations vs. maximizing revenue based on credit), higher integration costs, and leadership talent gaps—since fraud and compliance (or credit) require different skill sets.

Each of these models reflects a tradeoff. The important question isn’t which structure is “best,” but which one fits your organization’s business model, talent pool, and long-term goals.

Comparing Fraud and Risk Organization Models

As this comparison shows, every organizational model comes with clear tradeoffs. The key is not to look for a perfect solution, but to choose the approach that aligns best with your business priorities, growth stage, and team capabilities.

Pros and Cons of Each Organizational Setup

No matter which model you choose, there will always be tradeoffs. The key is to understand the benefits you’re gaining—and the risks you may be introducing—so that you can plan accordingly.

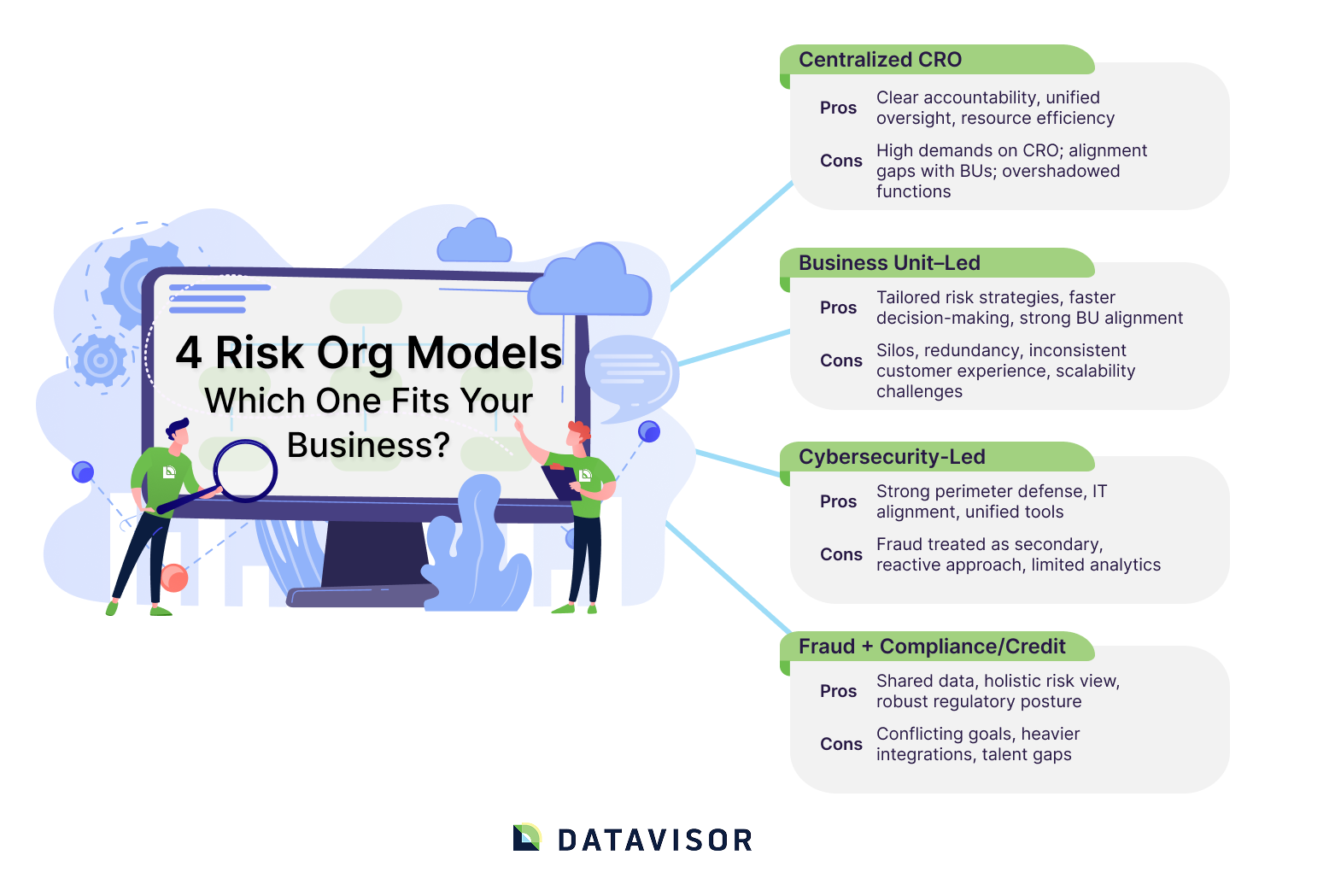

Centralized CRO Model.

- Pros: Clear accountability, stronger executive visibility, and the ability to reduce silos by unifying fraud, compliance, cybersecurity, and credit risk under one leader. This model often improves resource efficiency and promotes cross-team collaboration.

- Cons: It places very high demands on one individual, making it difficult to hire the right leader. Business units may feel disconnected from decisions, and some risk areas may be overshadowed depending on the CRO’s expertise.

Business Unit–Led Teams.

- Pros: Each unit can tailor its fraud and risk strategy to its own priorities, enabling faster decision-making and flexibility. This approach often works well for large, diversified organizations.

- Cons: The downside is duplication. Separate teams may adopt different tools, create silos, and deliver inconsistent customer experiences across products. Scalability also becomes a challenge.

Cybersecurity-Led Fraud Functions.

- Pros: Strong alignment with IT and cybersecurity practices, such as authentication and perimeter defense, often ensures resilience against account takeovers and bot-driven fraud.

- Cons: Fraud can become a secondary focus, with less emphasis on analytical skills and customer behavior insights. This often results in reactive detection rather than proactive prevention.

Fraud + Compliance (or Credit) Teams.

- Pros: Since fraud and AML (or credit) often share common data sources and infrastructure, combining them can improve efficiency and give institutions a more holistic view of suspicious activity. It also supports robust compliance in heavily regulated environments and more unified and consistent data analytics

- Cons: Conflicting goals—reducing fraud loss vs. meeting compliance obligations vs. maximizing credit revenue—can create tension. Integrations are more complex, and leaders with equal expertise in both domains are difficult to find.

Ultimately, no single approach is perfect. The right choice depends on your organization’s business model, geographic footprint, and talent availability. What matters most is being deliberate about the tradeoffs you accept.

Which Model Fits Which Organization?

Model

Pros

Cons

Best Suited For

Centralized CRO

Clear accountability, unified oversight, resource efficiency

High demands on CRO; alignment gaps with BUs; overshadowed functions

Mid- to large-sized institutions seeking strong top-down governance

Business Unit–Led

Tailored risk strategies, faster decision-making, strong BU alignment

Silos, redundancy, inconsistent customer experience, scalability challenges

Large diversified organizations with multiple products or geographies

Cybersecurity-Led

Strong perimeter defense, IT alignment, unified tools

Fraud treated as secondary, reactive approach, limited analytics

E-commerce companies or organizations where cyber risk dominates

Fraud + Compliance/Credit

Shared data, holistic risk view, robust regulatory posture

Conflicting goals, heavier integrations, talent gaps

Fintechs with strong analytics focus that can benefit from a shared infrastructure

With these tradeoffs in mind, the structure you choose is only part of the equation. Success also depends on the people within those teams—their mindsets, skillsets, and how well they align with the organization’s goals. In the next section, we’ll explore the distinct approaches and expertise required across fraud, cybersecurity, compliance, and credit risk functions.

Mindsets and Skillsets Across Risk Functions

Even the best-designed structure will fall short without the right people. Each area of risk—fraud, cybersecurity, compliance, and credit—requires its own mindset and skillset. Understanding these differences is critical to hiring, developing talent, and fostering collaboration across teams.

Cybersecurity

The cybersecurity mindset is centered on defense and protection. Practitioners focus on securing the perimeter, protecting data, and preventing intrusions before they happen.

- Mindset: Guard the gates, block intrusions, and respond quickly to incidents.

- Skillset: Threat intelligence, incident response, vulnerability management, and alignment with IT systems.

Fraud Prevention

Fraud professionals approach problems like detectives. Their goal is to identify anomalies, uncover hidden patterns, and stop losses before they escalate.

- Mindset: Investigate relentlessly, think like an adversary, and stay ahead of evolving schemes.

- Skillset: Advanced analytics, behavioral modeling, anomaly detection, and pattern recognition.

Compliance

Compliance requires a rule-bound and detail-oriented mindset. Teams must follow strict regulatory requirements, document every step, and ensure full auditability.

- Mindset: Precision over approximation, rigor over shortcuts.

- Skillset: Regulatory knowledge, audit and reporting expertise, policy enforcement, and governance processes.

Credit Risk

Credit risk management balances growth with prudence. It requires enabling lending and revenue opportunities while preventing large-scale losses.

- Mindset: Calculate risk vs. reward, empower growth while minimizing default exposure.

- Skillset: Risk modeling, portfolio analysis, data science, and a strong understanding of financial regulations.

When these diverse mindsets come together, they can complement one another. Cyber teams bring perimeter defense, fraud teams uncover schemes, compliance teams enforce rigor, and credit teams enable responsible growth. The challenge for leaders is ensuring these differences don’t create silos—but instead, reinforce a unified approach to managing risk.

Three Pillars for Any Effective Risk Structure

No matter which organizational model you choose, success depends on three common pillars. These serve as the foundation for building a resilient fraud and risk function that scales with your business.

1. Centralized Account Lifecycle Monitoring

Customers don’t see your organizational chart—they experience your institution as one entity. That means risk management must be consistent across the full customer journey. A centralized view of account activity enables teams to detect anomalies early, reduce friction, and ensure a seamless experience no matter the product or channel.

2. Shared Tools and Technology

Fragmented tools create fragmented insights. By adopting shared platforms and integrating data sources across fraud, compliance, cybersecurity, and credit, organizations can reduce redundancy, cut costs, and accelerate response times. Unified technology also lays the groundwork for advanced analytics and AI-driven detection.

3. Cross-Team Collaboration and Knowledge Sharing

Each risk function brings unique strengths. Cyber teams anticipate intrusions, fraud teams uncover schemes, compliance teams enforce rigor, and credit teams balance risk with growth. When these teams collaborate, they amplify one another. Sharing intelligence and best practices across functions not only strengthens defenses but also improves adaptability in a rapidly evolving threat landscape.

Together, these pillars ensure that risk management isn’t siloed, but integrated—enabling organizations to stay ahead of threats while maintaining efficiency and customer trust.

Choosing the Right Structure for Your Organization

So, which model should your organization adopt? The answer depends on your business nature, growth stage, and team capabilities. There is no universal solution—but there are guiding questions that can help you decide.

Consider Your Business Model and Risks

Start by asking: Which risks matter most to us? For fintechs and e-commerce companies, fraud and cybersecurity are often the dominant threats. For banks and lenders, credit risk and compliance obligations may take precedence. Your dominant risk exposure should heavily influence your organizational design.

Factor in Geographic and Product Complexity

If your business operates in multiple regions or offers diverse products, a one-size-fits-all risk function rarely works. Different geographies bring different regulatory requirements and fraud typologies. In such cases, business unit–led teams may provide the flexibility needed to adapt. But if your products and markets are tightly integrated, a centralized structure may offer a more consistent customer experience.

Assess Your Talent Pool and Leadership Strengths

The right model also depends on who you have—or can hire. If you have strong fraud and AML talent with overlapping expertise, a combined structure may work well. If your leaders are more specialized, separating risk functions may be more practical. Hiring a single leader with expertise across fraud, cyber, compliance, and credit is rare; recognizing your talent reality is critical to setting up teams for success.

Align Structure with Growth Goals

Finally, remember that your risk structure should evolve with your company. A startup may begin with a cybersecurity-led model, but as it expands into lending or new regions, it may need to shift toward a more centralized or hybrid approach. What matters is not locking into one model forever, but building flexibility to adapt as your risks evolve.

Final Considerations and Board-Level Imperatives

There is no silver bullet when it comes to fraud and risk organization. Every model carries benefits and tradeoffs, and the “right” answer depends on your business design, regulatory environment, and team capabilities. What matters most is being intentional—understanding your priorities, evaluating the skillsets you have, and preparing to adapt as your organization grows.

Increasingly, these decisions are no longer confined to operational teams. Fraud, cybersecurity, compliance, and credit risk are now board-level topics, with direct implications for financial performance and brand reputation. The way you structure your risk function can influence everything from customer experience to regulatory relationships. That’s why leaders at the highest level must engage in these discussions early and thoughtfully.

Finally, success depends on people. The best structure will fail without the right leaders and teams in place. Hiring and developing talent with the right mix of analytical rigor, regulatory knowledge, and cross-functional collaboration is critical. Organizations that invest here will not only prevent losses but also position risk management as a true strategic enabler.

Conclusion

Fraud and risk management are no longer just about preventing losses—they are about enabling growth. The way we design our organizations determines whether we’re constantly playing catch-up or proactively shaping a safer, stronger future for our businesses.

By choosing a structure that fits your business model, leveraging the right tools, and investing in the right people, you can transform fraud and risk from cost centers into strategic assets. These functions, when built thoughtfully, protect revenue, build trust, and create the foundation for long-term success.

As threats continue to evolve, so must our approaches. My encouragement to every leader is this: don’t wait until risk becomes a barrier to growth. Build the right foundation today, and your fraud and risk organization will not only defend your enterprise—it will help power its next chapter of growth.