Top 10 Fraud Platforms for 2026: Plus, Evaluation Criteria, Challenges, and Trends

Fueled by AI-powered scams, real-time payments, and the increasing complexity of global digital ecosystems, fraud is evolving faster than ever, pushing organizations to evaluate AI-powered fraud detection platforms capable of operating in real time.

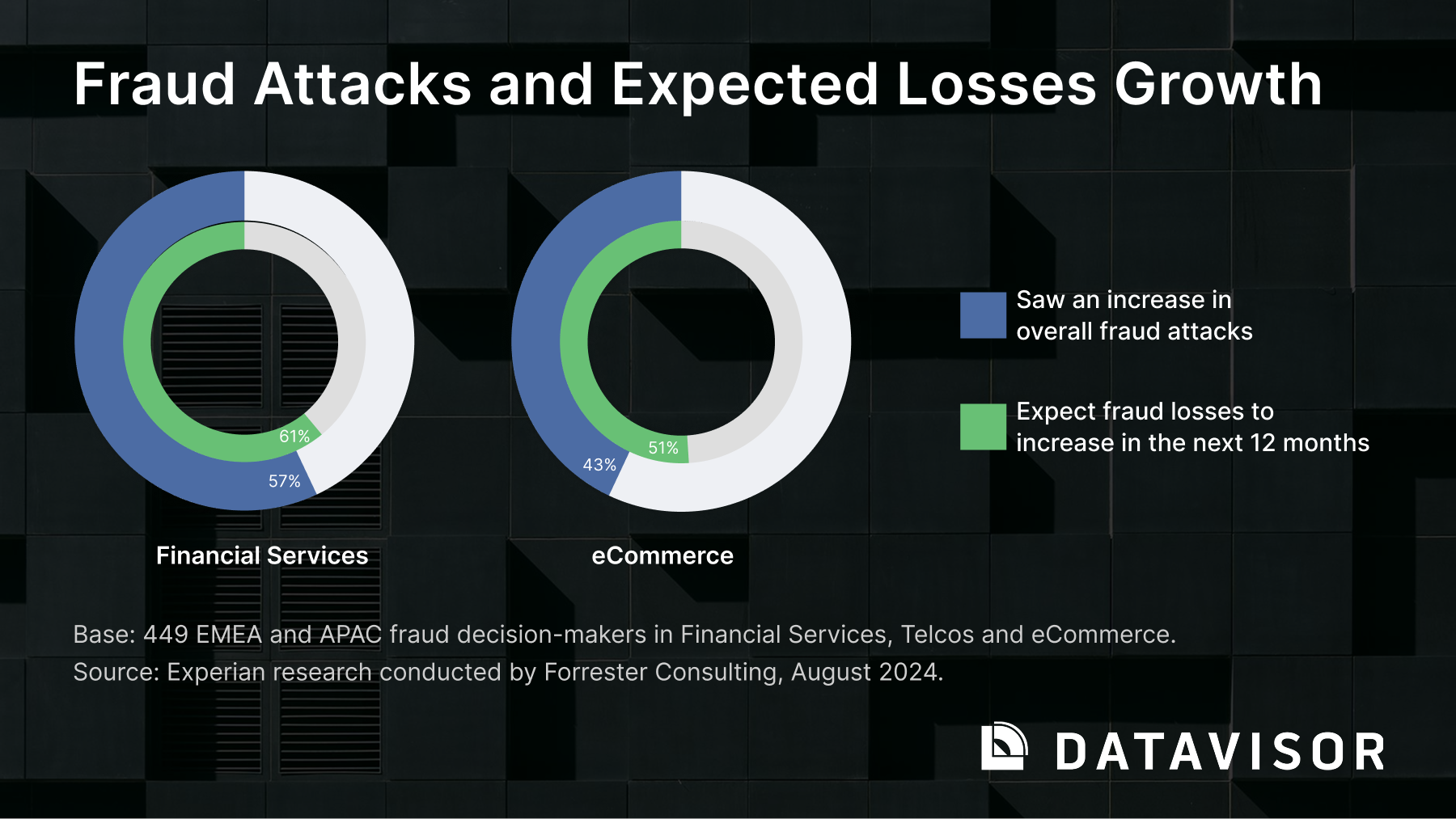

In 2025, the threat has never been more urgent: over $1 trillion in losses were reported globally last year, and just 4% of victims were able to recover their funds. Meanwhile, 93% of financial institutions cite growing concern over fraud attacks driven by artificial intelligence and generative AI.

In fact, according to Forrester Research, 61% of financial institutions expect the threat of fraud to grow in the coming year.

In this high-stakes environment, financial institutions and digital platforms face the challenge of stopping sophisticated fraud without disrupting the user experience. Choosing the right fraud detection platform is now critically important – and not just for security’s sake.

In this blog, we explore 15 leading fraud platforms shaping the future of fraud prevention, along with helpful considerations about what to look for when evaluating the right solution for your business.

7 Trends Shaping the Future of Fraud Prevention in 2026

As fraud becomes more automated, cross-channel, and AI-driven, organizations are rapidly modernizing their defenses. Several major trends are redefining what effective fraud prevention looks like in 2026, and shaping the technologies financial institutions, fintechs, and digital platforms are investing in.

1. AI as the Core Engine of Modern Fraud Detection

Artificial intelligence and machine learning have shifted from experimental add-ons to foundational components of fraud prevention. By 2026, a majority of enterprise fraud platforms are expected to rely on:

- Unsupervised ML to detect emerging and unknown fraud patterns

- Supervised ML to strengthen accuracy for known risks

- Generative AI for investigation summaries, rule recommendations, and alert triage

Link Analysis to assess entity relationships and uncover coordinated fraud rings

2. Device Intelligence, Behavioral Biometrics, and Continuous Authentication

Device intelligence and behavioral biometrics have become a mainstream defense for financial institutions and digital commerce. Today’s systems analyze:

- The use of emulators, VPNs, and hooks

- Typing cadence

- Touch pressure and swipe behavior

- Interaction speed and motion patterns

- Device handling signals

By early 2026, adoption of device intelligence, behavioral and biometric authentication continues to climb as organizations seek passive, low-friction ways to detect account takeover (ATO), social engineering, and human-in-the-loop fraud. These signals combined with session and transaction patterns, can significantly lift the effectiveness of verifying authenticity in real time.

3. Real-Time Fraud Controls for Instant Payments

The rise of instant and real-time payment systems — FedNow, RTP, Pix, UPI, SEPA Instant — has introduced new vulnerabilities. With near-zero room for manual review, organizations must rely on:

- Real-time risk scoring

- Pretransaction interdiction

- AI Behavioral risk models

- Mule account detection

- AI-driven social engineering detection

Fraudsters are exploiting payment speed to move funds quickly and irreversibly, making real-time intelligence mandatory.

4. Deepfakes, Synthetic Identities, and AI-Enhanced Social Engineering

Fintechs, neobanks, and digital marketplaces report growing exposure to:

- Deepfake voice scams

- AI-generated IDs

- Synthetic identity fraud

- Human puppeteering and coached social engineering

These attacks bypass traditional verification, pushing organizations to adopt document forensics, biometric liveness checks, contextual identity signals, and stronger multi-factor processes.

5. Rising Consumer Expectations

Consumers expect instant digital onboarding with minimal friction. This dual pressure is accelerating adoption of unified platforms that combine:

- Fraud detection

- Identity verification

- Case management and reporting

- Risk orchestration

Organizations must now optimize both rigorous detection and customer experience simultaneously.

6. The Shift Toward Unified Fraud + AML

One of the most significant transformations in 2026 is the move from siloed fraud and AML systems to integrated fraud & AML platforms. This unified approach provides:

- Cross-channel visibility

- Stronger detection of mule activity

- Fewer false positives

- Streamlined investigations

- Single case management workflows

- Consolidated reporting and audit trails

With fraud and AMLsignals increasingly overlapping, unified intelligence is becoming the industry standard.

7. Contextual and Behavioral Analytics at Scale

Organizations are placing greater emphasis on contextual signals — examining how, where, and why users behave the way they do. This includes:

- Location consistency

- Device reputation

- Network anomalies

- Relationship mapping

- Historical interaction patterns

This shift supports earlier detection of coordinated fraud, first-party abuse, and insider threats.

What These Trends Mean for Organizations in 2026

Together, these developments signal a decisive move away from reactive, rule-based strategies toward adaptive, AI-powered, unified fraud platforms capable of real-time detection and end-to-end orchestration. Organizations investing in flexible, intelligence-driven architectures will be best positioned to reduce losses, meet regulatory expectations, and protect the digital customer journey.

5 Challenges in AI-Driven Fraud Prevention for 2026

Fraud prevention in 2026 is entering a new era of complexity. Organizations across banking, fintech, and digital commerce are facing faster, more automated threats driven by AI, large-scale bot attacks, and increasingly sophisticated fraud rings. According to recent fraud research from Forrester and other industry analysts, agility remains one of the biggest challenges: most organizations still struggle to rapidly update fraud models, risk rules, or scoring logic when new attack patterns emerge.

1. Slow Response to Emerging and AI-Driven Threats

Fraud models and rule sets often take weeks or months to update, creating a dangerous gap between threat detection and response. Fraudsters now use automation, generative AI, and identity-mixing techniques to probe and exploit vulnerabilities at scale. Without real-time, adaptive defenses, organizations fall behind quickly.

2. Persistent False Positives and Customer Friction

False positives continue to be one of the most costly issues in fraud operations. Overly aggressive or outdated systems flag legitimate customers, leading to blocked transactions, onboarding friction, and lost revenue. These errors not only frustrate customers, erodes trust, slows growth, and creates an operational nightmare, slow growth but also erode customer trust, especially in high-velocity digital environments.

3. Challenges Operationalizing Machine Learning

Many institutions see the promise of machine learning, but struggle to operationalize it. Effective ML-based fraud detection requires:

- Clean, unified data

- Skilled data science resources

- Ongoing tuning and model monitoring

- Cross-system orchestration

Without these, ML becomes difficult to maintain and can inadvertently amplify noise.

4. Gaps in Device Intelligence and Identity Context

As a new wave of AI-driven identity fraud and account takeover (ATO) surge, organizations increasingly rely on device intelligence, location risk, behavioral analytics, and contextual identity signals. However, many teams lack deep device fingerprinting, behavioral sequencing or cross-channel visibility. Many times these signals are not integrated to the transaction workflow making it harder to distinguish legitimate customers from stolen identities, synthetic profiles, or coordinated bot activity.

5. Fragmented Fraud Tech Stacks and Orchestration Gaps

A common issue in 2026 is the reliance on a patchwork of disconnected tools, KYC solutions, bot mitigation, fraud scoring engines, case management systems, and systems that support one type of use case only (e.g., customer onboarding) — each solving a piece of the puzzle. When these systems don’t integrate well, teams lose:

- End-to-end visibility

- Cross-channel correlation

- Unified case investigations

- Ability to automate decisions

This fragmentation leads to inefficiencies, inconsistent decisions, and blind spots that attackers readily exploit.

These challenges highlight why many institutions are migrating to enterprise fraud management platforms that unify signals across identity, device, and behavioral analytics.

Why These Challenges Matter in 2026

Together, these challenges highlight the need for agile, AI-powered fraud platforms. In a landscape where attackers move with unprecedented speed, organizations must modernize their fraud architecture to stay ahead — or risk falling behind both competitors and increasingly sophisticated criminal networks.

Top 10 Fraud Platforms for 2026, Ranked

As fraud becomes more automated, networked, and AI-driven, organizations are turning to enterprise-grade platforms that deliver end-to-end visibility and real-time decisioning.

This ranking focuses on comprehensive fraud platforms—those that unify data, signals, and AI to stop fraud at scale. Each vendor was assessed on its innovation velocity, depth of machine learning capabilities, real-time performance, and enterprise adoption.

Below are the ten platforms that stand out for their ability to help organizations detect, prevent, and respond to today’s rapidly evolving threats. These are the top 10 fraud prevention platforms shaping the industry in 2026.

1. DataVisor

DataVisor is the industry’s leading AI-powered fraud and AML platform, built to help financial institutions and fintechs detect and stop sophisticated attacks in real time. Its unified architecture brings together fraud detection, AML monitoring, KYC/KYB workflows, case management, and risk decisioning into a single enterprise platform – eliminating silos and giving risk teams complete visibility across the customer lifecycle.

What differentiates DataVisor is its multi-layered AI engine, combining proprietary Unsupervised Machine Learning (UML), supervised models, link analysis, and agentic and gen AI that automate investigations and rule tuning. This ecosystem enables organizations to adapt rapidly to emerging fraud tactics, reduce operational workload, and improve investigation consistency without relying solely on historical labels or rigid rules.

Trusted by global banks, high-growth fintechs, and digital platforms processing billions of events per day, DataVisor is recognized for both its technical depth and its ability to scale to the world’s largest, most complex fraud and AML programs.

DataVisor ranks #1 as the only platform combining patented UML, unified fraud & AML, AI automation, and cloud-native scale into one enterprise fraud ecosystem. As the only unified fraud and AML platform on this list, DataVisor stands apart in both breadth and depth.

Strengths

- Proactive Detection with Patented UML + Unified Intelligence

DataVisor’s patented UML engine detects coordinated and previously unknown fraud patterns, offering early warning against new attacks, mule activity, and fraud rings. Combined with a unified graph and multi-signal decisioning, it provides a comprehensive view of risk across accounts, devices, transactions, and behaviors. - End-to-End Fraud + AML in One Platform

DataVisor delivers full fraud and AML capabilities, including real-time transaction monitoring, case management, alert triage, KYC/KYB workflows, risk orchestration, and automated SAR narrative generation. Everything is connected in a single workspace that removes data fragmentation and accelerates investigations. - AI Agents for Analyst Productivity

AI-powered agents automate repetitive tasks such as rule tuning, feature creation, and alert summaries. Interactive checklists guide analysts step-by-step through investigations, ensuring consistent, auditable outcomes and reducing time spent per alert. - Cloud-Native Speed & Scale

Built on modern cloud architecture, DataVisor supports millisecond-level scoring across billions of events. Enterprises can scale elastically, deploy rapidly, and adapt their workflows and models without downtime.

Potential Considerations

- Strategic Onboarding for Maximum Value

Because the platform is highly configurable and enterprise-grade, onboarding may require dedicated alignment on data integration, workflows, and model strategies. Organizations that invest upfront typically see substantial long-term performance gains. - Best Fit for Teams with Defined Fraud & AML Programs

DataVisor is designed for institutions with established risk practices looking to modernize or consolidate their fraud and AML stack. Its advanced capabilities are particularly powerful for organizations ready to take a strategic, analytics-driven approach.

Best Suited For

DataVisor is best suited for large financial institutions, digital banks, payment processors, and fintechs managing complex fraud and AML operations. It excels in environments where scalability, real-time decisioning, and cross-functional intelligence are critical—particularly for teams seeking to replace legacy rule-based systems with an adaptive, AI-first platform that learns continuously from evolving data.

2. Feedzai

Feedzai is an enterprise fraud platform, adopted by global banks and payment processors for real-time risk scoring and financial crime management. Its RiskOps platform uses supervised machine learning and rules orchestration to monitor transactions, detect anomalies, and support compliance-driven workflows across fraud, AML, and risk operations.

Strengths

- Enterprise-Grade Risk Platform

Proven scalability and reliability for high-volume financial institutions. - Flexible Rules & Model Management

Allows tuning and segmentation by product or geography. - Integrated Case Management

Built-in workflows for investigations and compliance reporting.

Potential Considerations

- Primarily uses supervised models, requiring continuous retraining with labeled data.

- Batch-oriented architecture can limit agility for real-time response to new or unseen fraud patterns.

- May require extensive engineering resources for configuration and model deployment.

Best Suited For

Large banks and payment providers needing a robust, compliance-aligned platform for transaction fraud monitoring and risk orchestration across multiple business lines.

3. Featurespace

Featurespace is known for Adaptive Behavioral Analytics, a technology designed to learn normal customer behavior and detect deviations that signal fraud or financial crime. Its ARIC Risk Hub provides real-time transaction monitoring and risk scoring across cards, payments, and digital channels.

Strengths

- Adaptive Behavioral Modeling

Continuously refines profiles of customer behavior to detect anomalies. - Strong in Payments & Card Fraud

Particularly effective in authorization and transaction-level monitoring. - Data Visualization & Explainability

Offers detailed insight into behavioral shifts and model decisions.

Potential Considerations

- Focuses primarily on behavioral analytics, with limited orchestration or data unification capabilities.

- May rely on supervised data feedback loops, which can slow adaptation to first-time attacks.

- Less emphasis on end-to-end fraud and AML integration compared to unified platforms.

Best Suited For

Financial institutions and payment networks seeking advanced behavioral analytics for transaction-level fraud detection and customer profiling.

4. NICE Actimize

NICE Actimize is an established name in financial crime and compliance, providing modular solutions for fraud, AML, and trading surveillance. Its platform supports large, regulated institutions with configurable workflows, rules, and analytics tailored for complex organizational structures.

Strengths

- Comprehensive Financial Crime Coverage

Fraud, AML, sanctions, and surveillance in one suite. - Mature Case Management

Advanced workflow controls and regulatory reporting features. - Proven Scale

Deployed across some of the world’s largest financial institutions.

Potential Considerations

- Legacy deployment models may require heavy IT and professional services investment.

- Longer implementation timelines and complexity compared to modern SaaS platforms.

- Model refresh cycles and tuning may lag behind newer AI-driven systems.

Best Suited For

Global banks and large financial organizations with mature compliance teams and infrastructure seeking deep regulatory coverage and workflow customization.

5. Verafin

Verafin specializes in fraud detection and AML compliance for mid- to large-sized financial institutions, particularly within North America. Acquired by Nasdaq, it offers integrated monitoring for fraud, AML, and case management with a focus on collaboration and intelligence sharing across institutions.

Strengths

- Integrated Fraud + AML Monitoring

Streamlines alert management across financial crime domains. - Consortium Intelligence

Shared typology detection and cross-institution data insights. - Strong in Core Banking Integrations: Deep alignment with U.S. and Canadian financial ecosystems.

Potential Considerations

- Regional focus limits applicability for global financial institutions.

- Batch processing may introduce latency for real-time transaction monitoring.

- Designed primarily for community and regional banks, not high-velocity fintech environments.

Best Suited For

Regional and mid-sized banks prioritizing integrated fraud and AML oversight with strong regulatory alignment and consortium data benefits.

6. LexisNexis Risk Solutions (ThreatMetrix + Emailage)

LexisNexis Risk Solutions is a long-established player in digital identity and device intelligence, known for its global identity graph and deep fraud signal coverage. Through its ThreatMetrix device intelligence network and Emailage email risk analytics, the solution provides a multilayered view of identity and behavior across billions of transactions.

With one of the largest cross-industry consortiums in the market, LexisNexis helps organizations detect high-risk patterns early, link related entities, and distinguish legitimate users from coordinated fraud activity. Its signals are widely used across financial services, ecommerce, lending, and payments to strengthen identity verification and improve decision accuracy.

Strengths

- Global Digital Identity Graph

ThreatMetrix provides real-time intelligence from one of the world’s largest device and behavior networks, enabling accurate recognition of trusted users and fast detection of anomalies. - Emailage Intelligence

Combines email metadata, identity linkages, and behavioral patterns to assess risk with high precision and support onboarding, login, and transaction flows. - Comprehensive Coverage Across Industries

Broad network visibility across financial services, retail, travel, gaming, and fintech improves match accuracy and insight depth.

Potential Considerations

- Data Coverage Varies Regionally

Signal depth is strongest in North America, Western Europe, and parts of APAC; organizations with users in less-connected regions may see variable performance. - Signal-Only Solution

While powerful as an identity risk layer, the product requires integration into broader fraud or customer decisioning systems.

Best Suited For

Organizations needing high-quality device and identity intelligence to enhance their onboarding, authentication, and transaction fraud decisions – especially global enterprises handling high user volumes.

7. TransUnion TruValidate (incl. iovation)

TransUnion TruValidate provides identity, device, and behavior intelligence powered by the iovation consortium, which has decades of data across billions of devices and fraud events. The platform helps organizations identify risky devices, assess behavioral anomalies, and access shared fraud markers contributed by a global network of participants.

Known for its reputation-based device graph, TruValidate offers valuable insights for preventing account takeover (ATO), stopping mule activity, and reducing repeat fraud. It is widely adopted by financial institutions, fintechs, and digital service providers looking to layer trust signals into identity verification and transaction flows.

Strengths

- Robust Device Reputation Network

Iovation’s long-standing device consortium helps surface risk patterns linked to fraud rings, repeat offenders, and coordinated attacks. - Integrated Identity Signals

Combines device risk insights with TransUnion credit, identity, and behavioral data, creating a more holistic risk profile. - Strong for Account Protection

Particularly effective in detecting ATO, suspicious logins, and risk in recurring customer interactions.

Potential Considerations

- Requires Integration with Existing Workflows

TruValidate provides signals, not full decisioning; organizations must integrate the intelligence into broader fraud systems. - May Require Tuning for New User Populations

Reputation signals work best when device histories and behaviors are well established.

Best Suited For

Enterprises seeking an additional trust layer to support login, authentication, and transaction flows – especially those aiming to reduce ATO and repeat fraud using consortium-based device intelligence.

8. Sift

Sift delivers a digital trust and safety platform designed to prevent fraud, abuse, and payment risk across online businesses. Its machine learning models analyze behavioral patterns and transaction context in real time to stop account takeovers, chargebacks, and policy abuse.

Strengths

- Real-Time Risk Scoring

Instant assessments for account creation, login, and payment events. - Global Network Effects

Learns from billions of events across merchants and digital platforms. - Policy Abuse & ATO Prevention

Broad coverage beyond traditional payment fraud.

Potential Considerations

- Focuses primarily on ecommerce and consumer applications, not enterprise banking.

- Limited customization for highly regulated or multi-channel financial environments.

- Relies heavily on supervised models, reducing agility against novel or synthetic attacks.

Best Suited For

Digital commerce, marketplaces, and consumer platforms looking for low-latency, scalable fraud prevention with strong coverage for account and transaction abuse.

9. Riskified

Riskified is a leading ecommerce fraud and chargeback protection provider, focused on helping merchants increase revenue by improving authorization rates and reducing false declines. Operating on a guarantee model, Riskified assumes financial liability for approved transactions, providing merchants with predictable outcomes and reduced operational effort.

Using machine learning trained on billions of global ecommerce transactions, Riskified evaluates user behavior, identity attributes, device characteristics, and historical patterns to distinguish legitimate shoppers from fraudsters. Its value is strongest for enterprises processing large volumes of card-not-present transactions.

Strengths

- Chargeback Guarantee

Merchants pay only for approved orders, and Riskified covers fraud losses, offering financial certainty. - Revenue Lift Focus

Solutions emphasize maximizing approvals, not just preventing fraud, making it attractive to retailers sensitive to conversion rates. - Strong for Global Ecommerce

Broad dataset improves performance for cross-border buyers and high-risk categories.

Potential Considerations

- Best for High-Volume Merchants

Smaller merchants may find pricing or integration effort misaligned with their scale. - Model Transparency

As decisions are fully managed, visibility into underlying signals may be limited for teams wanting granular control.

Best Suited For

Large ecommerce businesses seeking guaranteed outcomes, higher approval rates, and outsourced fraud decisioning.

10. Signifyd

Signifyd provides ecommerce fraud protection, abuse prevention, and chargeback guarantees designed to help retailers reduce operational overhead and prevent losses from ATO, return abuse, and friendly fraud. Its decisioning engine evaluates identity, behavior, device, and order patterns to automate approvals in real time.

With increasing focus on policy abuse and post-purchase fraud, Signifyd extends risk protection beyond checkout into claims, returns, and account protection, making it a comprehensive option for omnichannel merchants.

Strengths

- Guarantee Model with Broad Coverage

Includes fraud, ATO, and various forms of abuse, reducing uncertainty for merchants. - Omnichannel Protection

Supports ecommerce, in-store, marketplace, and buy-online-pick-up-in-store (BOPIS) workflows. - Strong ATO Detection

Behavioral analytics help surface compromised accounts early.

Potential Considerations

- Less Suited for Heavily Regulated Verticals

The model is optimized for retail and may not align with financial services or digital goods risk policies. - Requires Volume for Maximum Accuracy

Performance strengthens with richer transaction histories and broader behavioral data.

Best Suited For

Retailers and DTC brands seeking a complete fraud and abuse prevention solution with guaranteed liability coverage.

Honorable Mentions

While the platforms above represent the top end-to-end fraud solutions for 2026, several additional providers play important roles in the broader fraud prevention ecosystem. The vendors below offer specialized strengths—from fintech-focused risk APIs to OSINT investigation tools—and are included as honorable mentions for their influence and relevance across key use cases.

SEON

SEON is a modern, API-first fraud platform widely adopted by fintechs, digital lenders, and high-growth online businesses. Known for its speed and modular design, SEON provides device intelligence, digital footprinting, behavioral analysis, and risk scoring through lightweight APIs that integrate quickly into onboarding, login, and transactional flows. Its low-code/no-code configurations make it appealing for teams seeking rapid deployment and continuous optimization.

Unlike traditional enterprise fraud suites, SEON excels as a flexible, developer-friendly layer that boosts identity risk assessment and fraud detection without heavy infrastructure requirements. While not as feature-deep as unified enterprise platforms, it remains a strong choice for organizations prioritizing speed, agility, and modern fraud signals during the early stages of the customer journey.

Kount

Kount, now part of Equifax, is a long-established fraud platform known for its global identity trust network, combining device intelligence, behavioral data, and network-level insights across billions of interactions. Widely used in ecommerce and digital commerce, Kount helps organizations identify trusted customers, streamline approvals, and prevent payment fraud and account abuse with real-time decisioning.

Its strength lies in identity trust scoring and a large global dataset that enhances accuracy across checkout, loyalty, and account flows. While not as customizable as enterprise-grade platforms designed for financial institutions, Kount remains a strong fit for merchants and digital brands seeking a proven, scalable fraud detection engine with broad data coverage.

ShadowDragon

ShadowDragon provides investigation-focused OSINT (open-source intelligence) tools used to uncover fraud rings, coordinated criminal groups, and external threat activity across the open web, social media, and dark web environments. The platform helps fraud and security teams map identities, relationships, and behavioral patterns that fall outside traditional transaction or device data.

While not a real-time fraud scoring engine, ShadowDragon excels as an intelligence and investigation layer that strengthens high-risk case escalation, organized fraud detection, and cross-border investigations. It is particularly valuable for teams dealing with large-scale criminal networks, mule activity, or external intelligence gaps.

Spec (Spec Protected)

Spec offers identity and session security designed to stop account takeover (ATO), credential stuffing, malware-driven fraud, and phishing-based attacks before they reach critical workflows. By analyzing device behavior, session metadata, and anomalous patterns in real time, Spec adapts authentication requirements to risk, providing step-up security only when needed.

Because Spec focuses on the login and session layer rather than downstream transaction fraud, it is best deployed as a protective front line—complementing, rather than replacing, a primary fraud platform. It’s a strong choice for organizations seeking lightweight, user-friendly ATO prevention with minimal friction.

Sardine

Sardine is an API-based fraud and compliance platform built for modern fintechs, neobanks, and payment innovators. Optimized for high-velocity money movement, Sardine combines behavioral analytics, device intelligence, identity signals, and real-time transaction monitoring to evaluate risk instantly during account funding, card transactions, P2P transfers, and wallet activity.

Focused primarily on fintech and payments rather than large enterprise banking, Sardine excels at fast integration and early-lifecycle risk prevention. While it lacks some of the depth and explainability of full enterprise fraud suites, it remains a compelling option for digital-first companies that need instant decisioning and compliance checks across rapidly moving payment flows.

2026 Fraud Platform Comparison Matrix

Today’s market is crowded with tools that claim AI-driven protection, but their capabilities vary widely—from single-use APIs to full-scale enterprise platforms. Evaluating vendors through measurable criteria—like latency, model adaptability, and workflow automation—helps separate tactical solutions from true strategic platforms.

DataVisor stands out for combining patented Unsupervised Machine Learning, Agentic AI, and a unified feature store that together power proactive, end-to-end protection.

The table below compares leading fraud detection providers across key evaluation criteria, including AI approach, decisioning speed, data infrastructure, and workflow integration.

| Vendor | Primary Focus | AI/ML Approach | Real-Time Decisioning | Feature Store | Case Management | Key Differentiator |

|---|---|---|---|---|---|---|

| DataVisor | Unified Fraud & AML Platform | Unsupervised + Supervised ML, Agentic AI | Sub-100ms, real-time scoring |

Native, reusable features |

Unified workspace |

Patented UML engine + Agentic AI for adaptive, unified FRAML defense |

| Feedzai | Enterprise Fraud & Risk Platform | Supervised ML | Near real-time |

Custom setup |

Integrated |

Enterprise-grade RiskOps orchestration for large banks |

| Featurespace | Behavioral Analytics & Transaction Fraud | Adaptive Behavioral ML | Real-time |

Not available |

Add-on module |

Behavioral profiling engine for payments and card fraud |

| NICE Actimize | Financial Crime & Compliance Suite | Rules + Supervised ML | Batch / near real-time |

Not available |

Mature workflow tools |

Established FRAML and regulatory coverage |

| Verafin | Fraud & AML for Regional Banks | Rules + Supervised ML | Batch |

Not available |

Unified |

Consortium intelligence and AML integration |

| LexisNexis | Digital Identity & Device Intelligence | Network-based ML models | Real-time |

Not applicable |

External integration |

ThreatMetrix global identity and device network |

| TransUnion | Device Reputation & Consortium Data | Reputation-based ML | Real-time |

Not applicable |

Add-on integration |

Long-standing device graph and shared fraud markers |

| Sift | Digital Trust & Ecommerce Fraud | Supervised ML | <200ms |

Not available |

Basic |

Real-time digital trust scoring and abuse prevention |

| Riskified | Ecommerce Fraud & Chargeback Protection | Ensemble ML models | Real-time |

Not available |

Proprietary |

Chargeback guarantee and revenue lift for merchants |

| Signifyd | Ecommerce ATO & Policy Abuse | Supervised ML | Real-time |

Not available |

Integrated |

Fraud + abuse protection with guaranteed coverage |

How to Choose the Right Platform in 2026

With so many fraud solutions on the market, choosing the right one comes down to aligning the platform’s strengths with your organization’s needs. Start by identifying your top fraud risks and evaluate how each platform addresses those challenges.

Look for a solution that not only fits your current requirements but can also scale with your operations and adapt to new threats as they emerge. A truly modern platform should offer flexible integration, robust AI capabilities, and a balance between automation and investigator control.

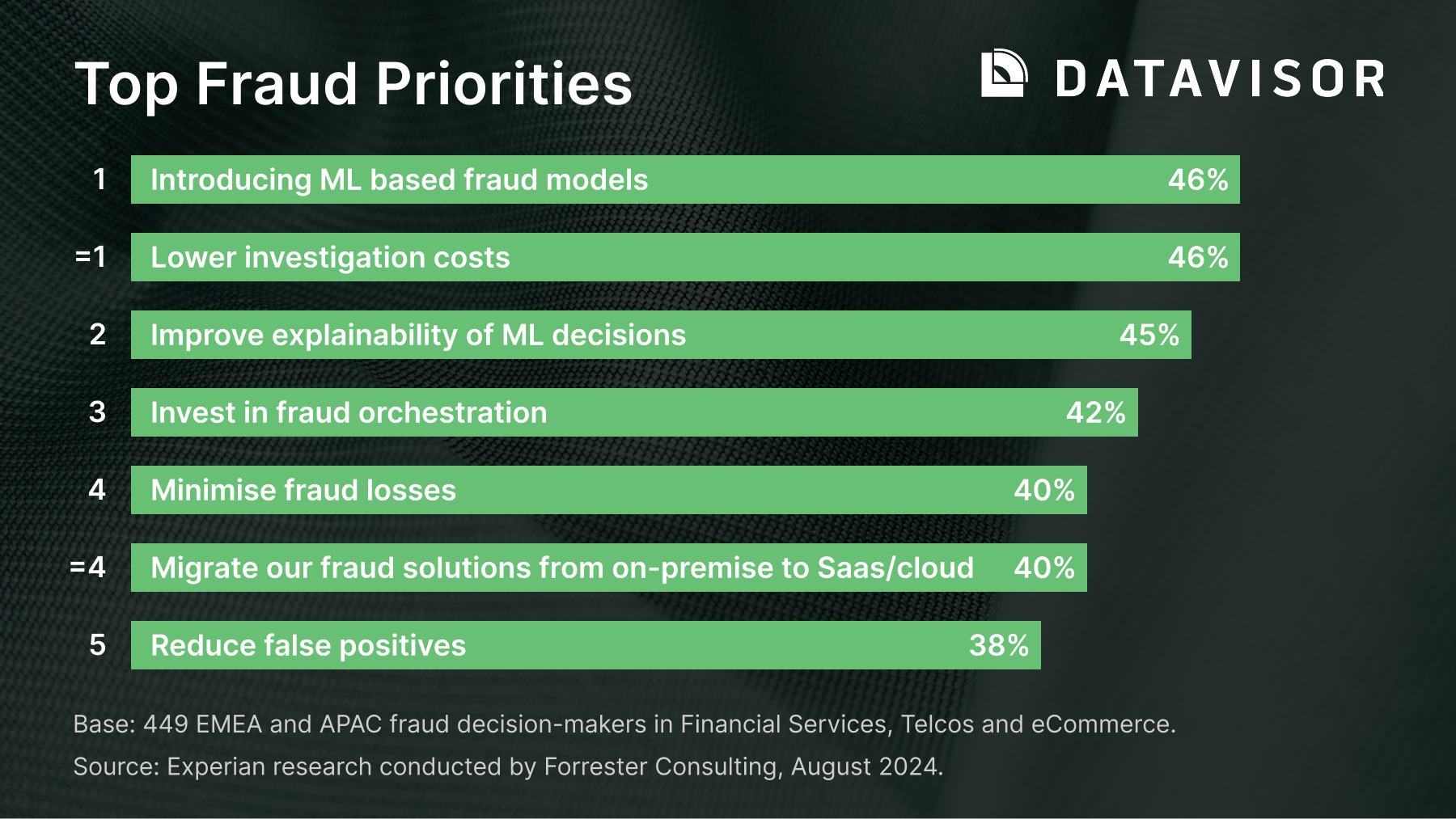

The table below shows the Top 5 priorities for the year ahead, according to Forrester.

7 Key Evaluation Criteria

When evaluating the best fraud detection platforms, organizations should look for capabilities that detect threats early, monitor continuously, and support analysts in responding efficiently — all while maintaining a seamless customer experience. Choosing a fraud solution in 2026 is no longer about finding a single tool. It’s about building the right defense architecture for your specific business model and risk profile.

The framework below encompasses the core evaluation criteria to guide your selection, whether you’re an established bank, large payment processor, or fintech start-up.

1. Customer Lifecycle Coverage

Fraud doesn’t occur at a single point. It unfolds across multiple touchpoints. A strong platform should provide visibility and risk control from onboarding through post-transaction review. Ensure your chosen platform covers (or integrates with tools that cover) every major touchpoint:

- Account creation and onboarding (including KYC integration)

- Authentication and login flows

- Transaction and payment risk assessment

- Continuous user monitoring and behavioral tracking

- Dispute management and post-event analysis

A strong platform should unify signals across these phases to create a single, risk-aware view of each customer.

2. Signal Breadth and Quality

Fraud prevention relies on the strength of its data. Evaluate the diversity and depth of signals the platform provides or integrates to detect anomalies.

Key signal types include:

- Behavioral patterns

- Device intelligence

- Digital identity linkage

- Graph-based entity relationships

- Document and biometric verification

- Bot and automation detection

Platforms that unify or orchestrate these signals typically provide the strongest precision, richer risk profiling, and resilience against new attack patterns.

3. Real-Time Data Orchestration

Modern fraud prevention requires breaking down data silos. Choose a platform that can unify, transform, and route signals from multiple systems in real time — including payment gateways, data lakes, KYC providers, and core banking systems.

Key capabilities include:

- Stream-based data ingestion and scoring

- Event correlation across channels and entities

- Flexible API and webhook integrations

- Real-time enrichment from third-party data sources

Effective orchestration ensures that intelligence flows seamlessly between systems, enabling faster decisions and more consistent outcomes.

4. Real-Time Transaction Monitoring & Decisioning at Scale

As payment systems accelerate, real-time decisioning has become non-negotiable. The best platforms deliver instant, high-volume scoring while maintaining precision.

- Sub-100ms decisioning latency

- High-performance, cloud-native infrastructure

- Pattern recognition across accounts and payment networks

- Mule account and social engineering detection

- Adaptive controls that trigger before funds move

Continuous transaction monitoring strengthens both fraud prevention and customer experience by reducing false declines and enabling immediate interdiction.

5. AI/ML Capabilities & Adaptability

Fraudsters now use AI to scale and evolve attacks — your platform needs to be equally adaptive. The most advanced fraud systems combine multiple AI techniques with transparent, explainable outcomes that balance accuracy and control.

- Unsupervised ML: Detects new and unknown fraud patterns without relying on historical labels.

- Supervised ML: Strengthens precision and recall for known risks.

- Generative AI: Automates alert triage, case summaries, and feature or rule recommendations.

- Agentic AI: Introduces autonomous, goal-driven agents that proactively optimize detection strategies, tune rules, and accelerate investigations — reducing manual overhead and response times.

- Graph Analytics: Reveals hidden connections between entities, uncovering coordinated fraud rings and mule networks.

- Adaptive Learning: Continuously retrains models using new data and analyst feedback to stay ahead of emerging threats.

Platforms that blend multiple AI techniques — and make results explainable — enable both agility and auditability.

6. Case Management & Analyst Productivity

Operational efficiency drives ROI. The right platform should empower analysts to resolve alerts faster and more consistently.

- Unified case views that aggregate all signals and actions

- AI-assisted summaries and guided investigation checklists

- Evidence capture and enrichment

- Automated alert routing and prioritization

- Audit-ready documentation and replayable decision trails

Effective case management turns detection into resolution, ensuring that insights translate into action. Solutions that improve analyst consistency and speed deliver major operational savings.

7. Cost Structure & Business Impact

Fraud prevention is a revenue enabler, not just a cost center. Assess each platform’s total impact on financial and operational outcomes, including:

- Reduction in fraud losses and chargebacks

- False positive improvement and approval rate uplift

- Analyst time saved through automation

- Lower infrastructure or licensing costs via cloud scalability

- Compliance and reporting efficiency

A platform that protects revenue, improves customer trust, and reduces operational drag delivers measurable ROI and long-term value.

These capabilities form the foundation of any effective fraud strategy.

Key Questions to Ask a Fraud Platform Vendor

Selecting the right fraud and risk platform is a strategic, long-term decision — one that impacts detection accuracy, operational efficiency, customer experience, and regulatory compliance. Before committing to a vendor, it’s essential to dig deeper into how the solution works, how it scales, and how it adapts to modern threats.

Below are the most important questions to ask during your evaluation.

1. Coverage & Detection Capabilities

- What types of fraud does your platform detect best?

(ATO, synthetic identity, first-party fraud, social engineering, bot attacks, payment fraud, money mule activity, etc.) - How do you handle cross-channel visibility and lifecycle coverage?

(Account opening → login → payment → continuous monitoring)

2. Performance, Latency & Scale

- How quickly can your system process and respond to high-volume, real-time transactions?

- Is your architecture cloud-native and elastically scalable to support surges in volume?

- What are your uptime, performance, and SLA guarantees?

3. Adaptability to Emerging Threats

- How does your platform detect previously unseen fraud patterns?

(Unsupervised ML, anomaly detection, link analysis, AI agents) - How often are models updated, and who controls those updates — your team or ours?

- How do you incorporate new signals or data sources?

4. Explainability, Controls & Business User Empowerment

- Can risk teams adjust rules, thresholds, or workflows without engineering support?

- How transparent and explainable are your ML models and risk scores?

(Important for compliance, auditors, and regulators)

5. Integration, Orchestration & Data Requirements

- What does the integration process look like, and what systems do you typically connect with?

- Can your platform orchestrate signals from other tools (KYC, device intelligence, bot mitigation, etc.)?

- What data do we need to provide at minimum to get started?

6. False Positives & Customer Experience

- How do you minimize false positives while maintaining high detection accuracy?

- Do you support A/B testing, model comparisons, or dual running before going live?

- What controls exist to reduce friction for trusted users?

7. Compliance, Auditability & Unified Intelligence

- How do you document investigation steps and decisions?

- How do you ensure auditability and explainability of decisions?

- Do you support unified data, risk signals, and case insights to provide a consistent view of suspicious activity across Fraud & AML?

8. Deployment, Pricing & Ongoing Support

- What is your typical deployment timeline and onboarding process?

- What does your pricing model look like (usage, events, seats, tiers)?

- What support is included, and do you offer dedicated success resources?

Navigating the Future of Fraud Prevention

Fraud prevention today demands agility, intelligence, and seamless integration across systems. As threats grow more complex and real-time payment environments leave little room for error, you need a solution that can identify fraud quickly, accurately, and at scale. The right platform for your organization will depend on a range of factors, from your size and industry to your data infrastructure and regulatory landscape.

With its proprietary AI engine, unified fraud & AML capabilities, and cloud-native orchestration, DataVisor delivers the speed, scalability, and precision modern institutions need. It empowers teams to respond to threats in real time while reducing false positives, and future-proofing their fraud strategies.

Explore how DataVisor can help you stay ahead of evolving fraud threats. Request a demo or contact us today.